Close Menu

Want to authorize more?

50% of declines from card issuers are due to insufficient funds. Riskified’s report from 2019 revealed that most customers who receive NSF declines are actually “life events” shoppers and travelers. Life events include larger payments for wedding planning, moving to a new home, or having a baby. Regrettably, this is the most inconvenient time for those individuals to deal with such a hassle.

Usually, consumers don’t know whether merchants or issuer banks are to blame for payment declines, especially if they have the money. But when the reason for the decline is insufficient funds, frustrated customers tend to blame the issuing bank. Depending on their level of frustration, they call the bank to complain. They might ask for a credit increase, or even cancel their card. Worst case, they’ll use another card or a different payment method — regardless, the card issuer will lose the top of wallet position.

While credit cards have credit limits for a reason, they also know their good customers. What if you could give your good customers a pass and approve the transaction even though it’s over the credit limit? What if you could do it without added risk? With Kipp, you can.

When a transaction is falsely declined, consumers “punish” the bank by using another card for subsequent transactions, causing banks to lose even more revenue. Unlike declines due to failed validation, payment declines due to insufficient funds are an entirely different ball game. The risk in approving the transaction is loss, not fraud. Fortunately, issuer banks know how to assess and price risks. Unfortunately, they can’t do it in real-time or per transaction.

The decision to approve or decline a transaction due to insufficient funds is a question of risk vs. reward. On the one hand, you risk financing a ‘loan’ the customer won’t repay. On the other hand, the reward of having a satisfied customer who got what they wanted and paid the bill on time like they always do.

The booming Buy Now Pay Later markets methods are the go-to solution for many shoppers that couldn’t complete their transactions because the bank declined them. Yet, they managed to grow into a $20.40 billion market. So the question is, can banks afford to keep declining NSF transactions across the board?

If banks have enough data to define their good customers and they can price the risk of approving a payment despite “insufficient funds,” the remaining challenge is covering the risk cost.

Well, that’s the idea behind Kipp’s solution.

Kipp offers an innovative approach to managing real-time risk assessment and compensation on every transaction without human interaction. Kipp leverages the aligned interests of issuing banks and merchants to authorize more legitimate transactions by having the merchants cover the risk cost, which is typically assumed only by issuers.

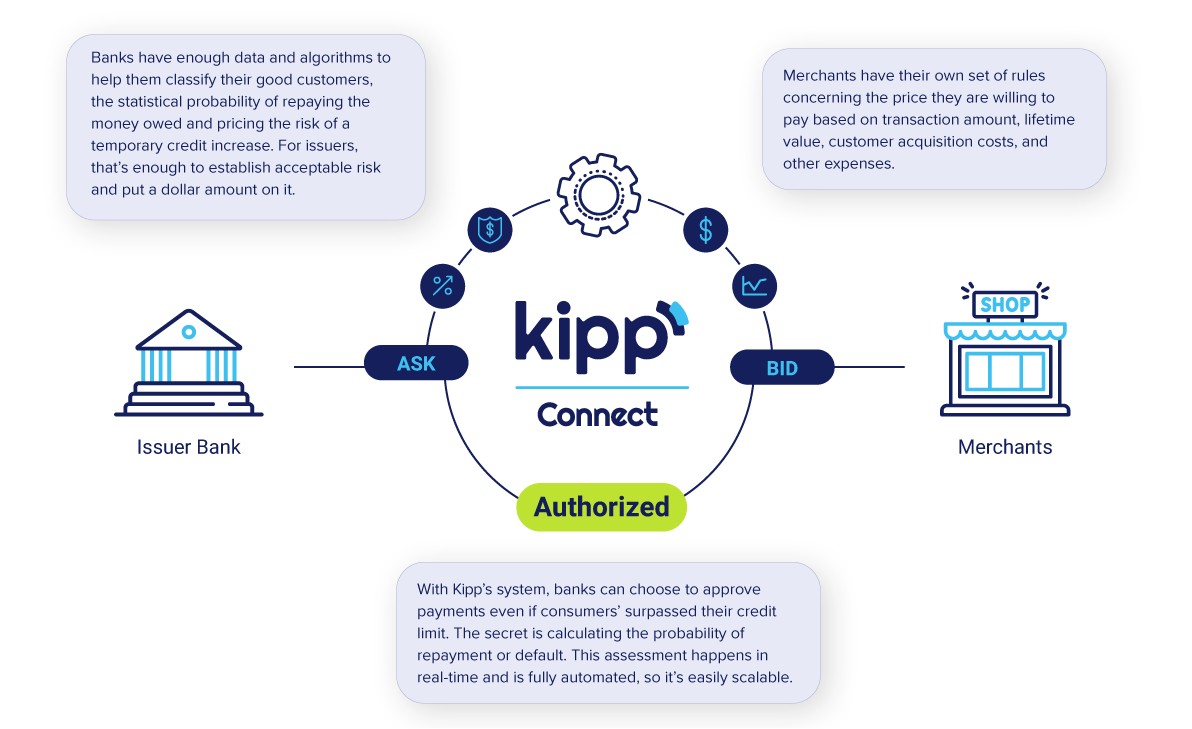

The diagram below illustrates Kipp’s role and position between the merchants and issuer banks.

Banks have enough data and algorithms to help them classify their good customers, the statistical probability of repaying the money owed, and pricing the risk of a temporary credit increase. For issuers, that’s enough to establish acceptable risk and put a dollar amount on it.

Similarly, merchants have their own set of rules concerning the price they are willing to pay based on transaction amount, lifetime value, advertising, and other expenses.

With Kipp’s system, merchants can automatically agree to the compensation card issuer’s offer in order to approve the payment. This exchange happens in real-time and is fully automated, so it’s easily scalable.

With Kipp’s help issuing banks can significantly reduce operational costs associated with complaints and instead increase payment approvals, revenue, and customer satisfaction. Kipp’s solution meets the needs of card issuers, merchants, and customers of the digital age by optimizing the traditional payment model.

Kipp created a solution that provides more loyal customers for card issuers and merchants by covering the risk cost using the world’s first automated communication channel. Helping banks replace the embarrassing moments of declined transactions with a seamless solution that optimizes payments. Thankfully, Kipp works with all issuers, so if you want to start optimizing payment authorization to increase customer loyalty, click here to get started.