Close Menu

Want to authorize more?

Issuers incorrectly decline transactions causing them to lose revenue from interchange fees. Kipp can help issuers approve 50% of the transactions that they currently decline.

In today’s climate, any sign of risk causes card issuers to decline transactions automatically – a smart and justified decision for banks that want to protect themselves and their customers from fraudulent activity. But the reality is far more complex.

Ironically, declining legitimate transactions doesn’t just cost card issuers and merchants a lot of money and lost revenue. It’s enough to decline one transaction to lose the top of the wallet position. But more than anything, false positives push away good customers, damage issuing banks’ reputation and customer satisfaction rates, which are tough to repair or quantify.

But what if card issuers could bring themselves to optimize their payment approval rates without the added risk?

More often than not, legitimate transactions are declined because of failed validation checks. While validation is an important and delicate step in the payment authorization process, it can easily fail. Take for example the CVV mismatches, or the expiry date mismatches. These reasons are not really an accurate indication of fraud by all accounts but they do impose a certain risk.

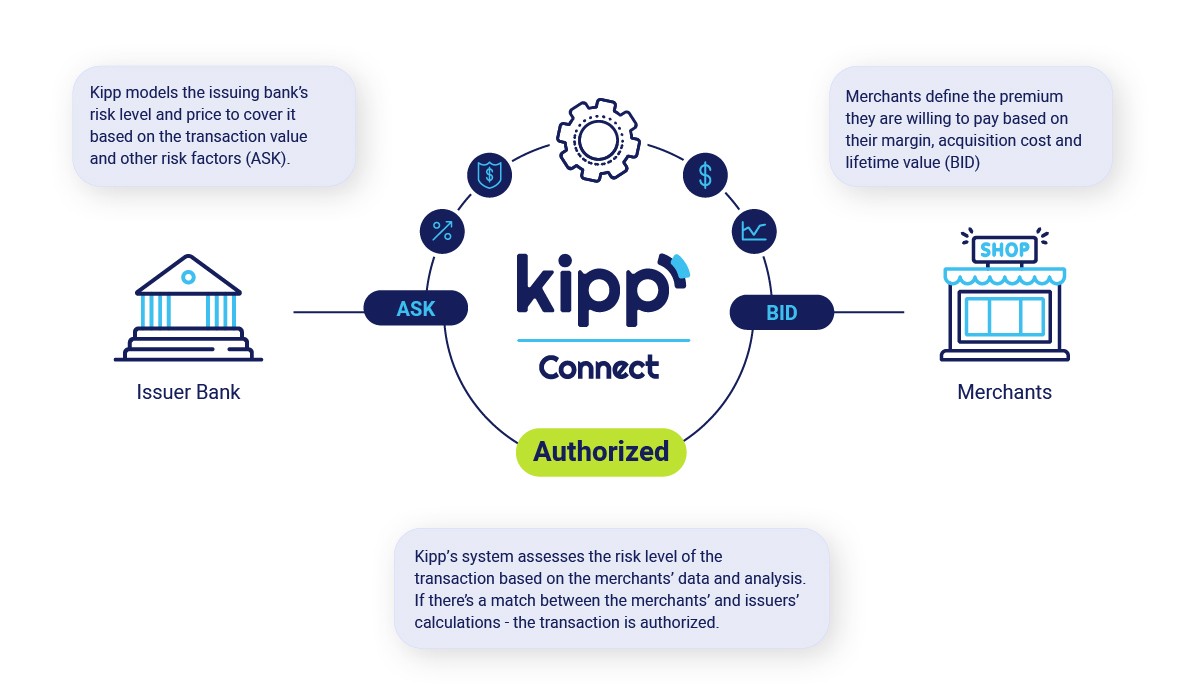

So how can issuing banks approve more legitimate transactions instead of helplessly watching their revenue and customers go to their competitors? With Kipp’s help, bank issuers and merchants can work together to optimize their payment authorization process.

While the policies are different among banks, they all share the same objective, mitigating losses. As for the merchants, their interest lies in approving their customers’ payments to increase their revenue.

Suppose the merchant can be allowed to partake in the risk cost to approve the payment and maintain their customers’ loyalty and satisfaction. In some cases, they will gladly pay to authorize the transaction even if the validation step fails. Because they know who their good customers are.

The only thing missing in bringing this vision to life is a third-party solution that can facilitate this exchange of information in real-time.

Meet Kipp.

Realizing issuing banks and merchants have shared interests, Kipp created a way to optimize the payment authorization process without added risk. By creating new communication and automatic decision-making channel for merchants and issuing banks.

The following is what happens every time a Kipp customer “swipes” their card successfully and is unaware that they almost got declined:

Authorizing more legitimate transactions boosts customer satisfaction and reduces complaint calls and the costs and frustration associated with them. By giving customers what they want, when they want it you will be rewarded with much more than the transaction amount. You will be rewarded with customer loyalty.

Don’t worry. While it takes a few paragraphs to explain how Kipp works, the authorization process takes only a fraction of a second from start to finish. Kipp works with all banks, so if you want to optimize your payment authorization process and gain more satisfied customers, click here to get in touch.